Health Insurance

National Health Claims Exchange: A Quiet Revolution in Health Insurance

How NHCX is transforming India’s health insurance claims infrastructure through standardization and digital innovation.

Recalibrating the Claims Infrastructure

Health insurance in India has undergone steady reform over the last decade, but one operational challenge has persisted: the claims process. Today, claims remain fragmented, resource-intensive, and opaque both for hospitals submitting them and for policyholders awaiting resolution. Despite digital touchpoints, much of the process is still manual, with providers engaging multiple portals, insurers chasing documentation, and patients navigating uncertainty. For a system tasked with offering financial assurance in medical crises, the underlying infrastructure is overdue for systemic overhaul.

RNHCX: A Public Digital Rail for Claims

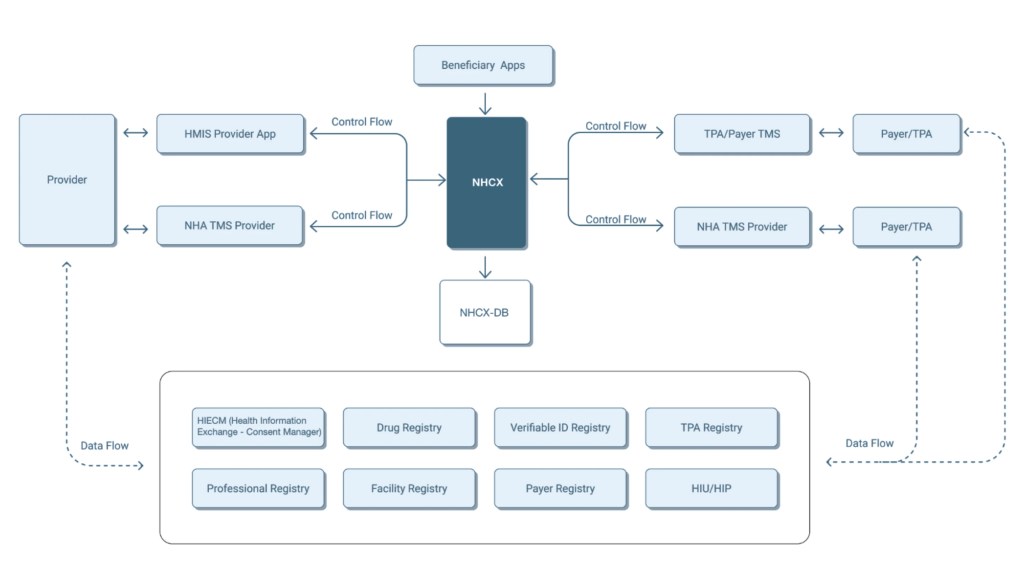

The National Health Claims Exchange (NHCX), developed by the National Health Authority (NHA) in collaboration with the Insurance Regulatory and Development Authority of India (IRDAI), is designed to address this very problem not by digitizing old workflows, but by replacing them with a standardized, interoperable, and consent-based claims network. Built on globally recognized FHIR standards and integrated with the Ayushman Bharat Digital Mission (ABDM), NHCX provides a single API framework that facilitates real-time claim exchange between hospitals, insurers, and third-party administrators.

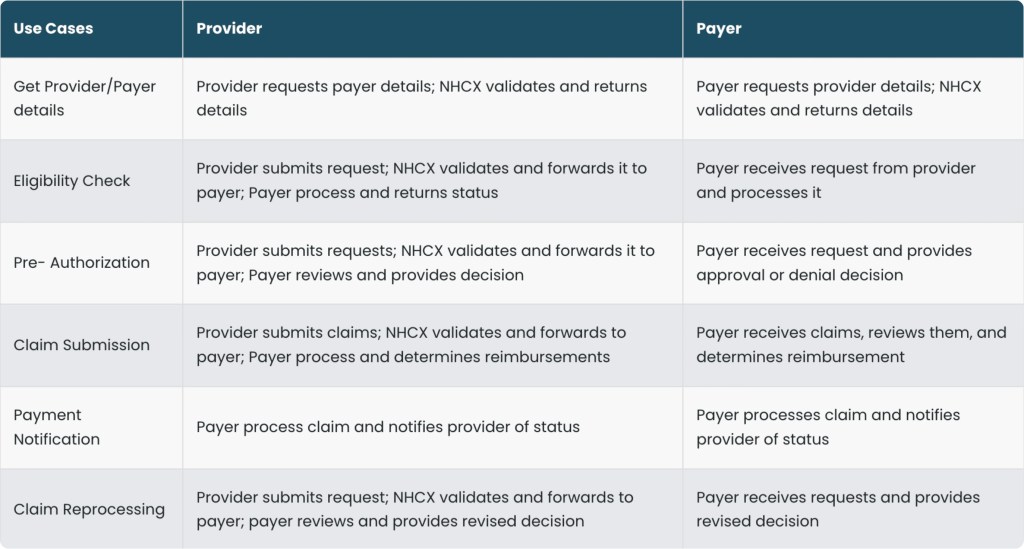

The logic is simple but transformative: instead of managing fragmented interfaces, hospitals submit claims once through NHCX, which validates, structures, and routes them directly to the correct insurer. The entire lifecycle from coverage verification to pre-authorization, final claim, and settlement—is handled through a single protocol. This architecture not only enables straight-through processing but also ensures that patient, provider, and policy data are reliably authenticated via national registries like ABHA, HFR, and HPR.

Operational Impact and Ecosystem Efficiency

The implications of NHCX’s implementation are wide-reaching. Hospitals can now reduce the cost and complexity of claims management by eliminating redundant portals and process overhead. Insurers, in turn, gain access to structured, machine-readable data, allowing for faster adjudication, improved fraud detection, and consistent service standards. Early pilot reports suggest claim processing costs could fall from ₹500 to under ₹15 per transaction, creating operational headroom to expand coverage especially for OPD, diagnostics, or preventive care services that were previously administratively unviable.

For TPAs, the platform reduces integration fatigue, while for regulators, NHCX enables real-time performance visibility claims approval times, rejection reasons, fraud patterns at a level of granularity previously inaccessible. Perhaps most significantly, for policyholders, the process becomes transparent, traceable, and time-bound. Discharge delays reduce. Communication improves. Confidence is restored.

Industry Participation and Rollout Progress

Adoption has been remarkably swift for an initiative of this scale. As of mid-2024, more than 47 insurers and TPAs representing nearly the entirety of India’s retail health insurance market have connected to the NHCX sandbox or live environment.

Importantly, this scale-up has occurred without regulatory mandate. IRDAI’s strategy has focused on collaborative enablement rather than enforcement, complemented by a series of technical workshops, stakeholder roundtables, and capacity-building sessions. The result is an ecosystem-wide alignment on standards and intent an uncommon feat in Indian financial infrastructure development.

Beyond Claims: Strategic Leverage for Insurers

NHCX is not a claims tool; it’s a strategic asset. For insurers, the implications extend far beyond efficiency. Standardized, codified claims data unlocks powerful underwriting, actuarial, and product innovation capabilities. Over time, integration with ABDM’s Personal Health Records could allow for risk-based pricing or outcome-based reimbursement.

Furthermore, the availability of transparent benchmarks claim turnaround times, approval consistency, hospital performance will enable differentiated service propositions and internal accountability. It also builds a national repository of anonymized, high-fidelity claims data, which can inform public policy, detect epidemiological trends, and refine treatment guidelines.

A View Forward

Looking ahead, NHCX is poised to become the default transaction layer for all health insurance claims in India. The roadmap includes onboarding a broader set of providers, expanding to outpatient and pharmacy claims, integrating with payment systems for direct reimbursements, and embedding NHCX within digital health journeys like teleconsultation and home care.

Importantly, NHCX sets the stage for regulatory interventions that are data-informed and service-oriented. Time-bound cashless approvals, grievance redressal through verified logs, and service-level benchmarking are all now within reach. The exchange also opens the door to international learnings comparable to clearinghouses in the US or EHDS initiatives in Europe but with the added advantage of central design and open standards from inception.

Conclusion: Infrastructure That Quietly Changes Everything

Like many digital public goods, NHCX is infrastructure that isn’t meant to be seen it’s meant to be experienced through everything it improves. When a patient is discharged three hours sooner, when a hospital administrator files fewer follow-ups, or when an insurer adjudicates 1,000 claims per day without scaling staff NHCX is the quiet engine enabling it.

For insurers and providers alike, this is the moment to not only integrate technically, but to evolve operationally and strategically. Claims, once viewed as cost centers and compliance burdens, can now become levers of service, trust, and insight. In that sense, the National Health Claims Exchange may well be India’s most significant health insurance reform in a generation one that redefines what claims infrastructure should do, and how simply it should do it.

Recent Posts

Related Posts

RegTech & Compliance: The Future of Digital Insurance in India

India Insurance Sector: Too Few for Too Many | Insurtech 2025

DPDPA Meets AI: Regulating the Future of Intelligent Insurance

DPDPA in Indian Insurance | Building Customer Trust & Digital Agility

India’s Health Protection Gap: Fixing Coverage for Gig Workers