Insurance Innovation

Sandbox to Scale: How IRDAI is Driving Insurance Innovation

How IRDAI’s Regulatory Sandbox is helping insurers test, validate, and scale breakthrough ideas in India’s evolving insurance ecosystem.

India’s insurance sector has long operated within rigid, product-driven regulatory boundaries. While this ensured policyholder safety, it often left little room for experimentation. That changed in 2019, when the Insurance Regulatory and Development Authority of India (IRDAI) introduced its Regulatory Sandbox framework, a bold step to balance innovation with supervision.

The sandbox concept, already adopted by financial regulators in banking and payments, offered insurance players a similar opportunity: to test innovative ideas under relaxed regulations in a time-bound, controlled environment. This was not deregulation, it was de-risked innovation with regulatory visibility, consumer safeguards, and learning outcomes built in. For an industry seen as risk-averse, this signaled a clear shift in mindset, from reactive compliance to proactive transformation.

How the Sandbox Works

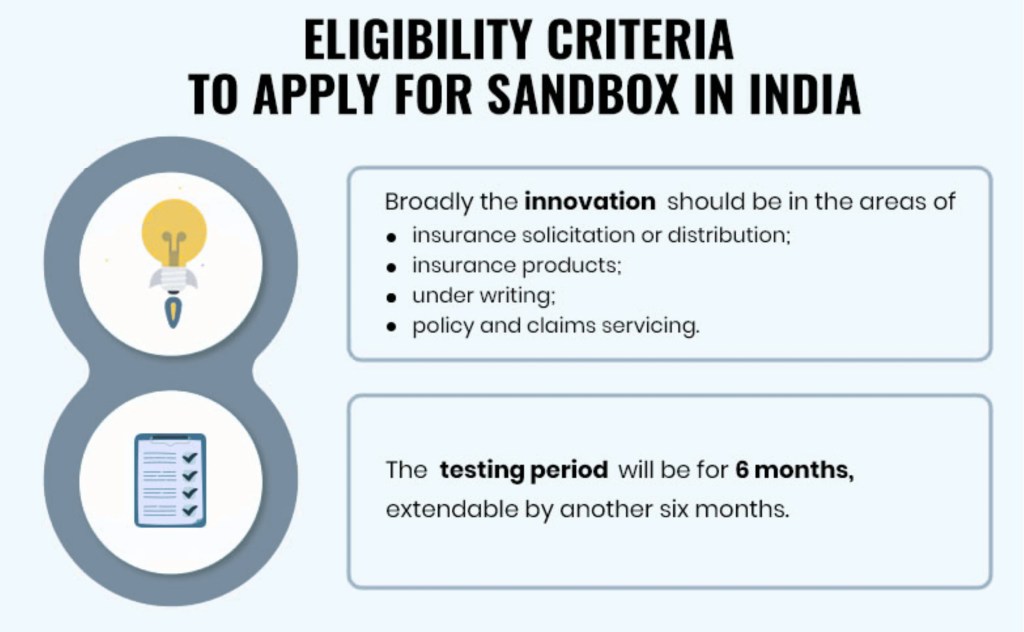

Under the sandbox, insurers, intermediaries, or insurtech startups (in partnership with insurers) can apply to test new products, underwriting models, service workflows, or distribution methods. If approved, they’re allowed to run a pilot for up to 12 months, with temporary regulatory relaxations such as modified product rules or KYC flexibility.

Each test has well-defined boundaries—no more than 10,000 customers or ₹50 lakh in total premium. The scale is small, but the learning is large. After the pilot, the product is evaluated for safety, utility, and impact. If it passes, IRDAI may allow it to scale under standard regulations. If it fails, the damage is limited and controlled. This framework gives the industry a safe space to experiment, iterate, and innovate without systemic risk.

What the Sandbox Enabled

Across its first two cohorts, IRDAI received over 350 applications, spanning motor, health, distribution, and servicing. The diversity of ideas validated one thing: innovation in insurance is not scarce, it just needed a platform.

Usage-based motor insurance was one of the most prominent themes. Insurers like Go Digit and ICICI Lombard tested “pay-as-you-drive” or “pay-how-you-drive” models, using telematics to calibrate premiums based on driving behaviour or mileage. These were ideas long considered unfeasible under traditional product structures.

In health insurance, the sandbox enabled wellness-linked plans, wearable integrations, and incentive-based covers. Companies partnered with health-tech platforms to offer discounts based on activity data, or rewards for healthy group behavior’s. Bajaj Allianz, for example, piloted a motor claim model (V-Pay) that enabled instant settlements via app-based verification.

For TPAs, the platform reduces integration fatigue, while for regulators, NHCX enables real-time performance visibility claims approval times, rejection reasons, fraud patterns at a level of granularity previously inaccessible. Perhaps most significantly, for policyholders, the process becomes transparent, traceable, and time-bound. Discharge delays reduce. Communication improves. Confidence is restored.

What Actually Scaled

The sandbox is only as impactful as the ideas it helps bring to market. And in that regard, it has delivered.

Take usage-based insurance, once seen as too complex for regulation, it is now allowed outside the sandbox. In 2022, IRDAI formally permitted insurers to launch telematics-based add-ons like Pay-as-you-drive and Pay-how-you-drive. That policy shift was rooted in the data and validation generated by sandbox pilots.

Similarly, wellness-linked products have gained regulatory clarity. Some sandboxed health covers that rewarded customers for fitness engagement are now active products. Toffee Insurance’s dengue and cycle theft covers, once niche sandbox pilots, are now distributed at scale through embedded platforms and digital brokers.

Even operational workflows have evolved. Video-based or app-based motor claims, tested under the sandbox by firms like Bajaj Allianz, are now standard in their processes. The customer experience is faster, digital-first, and less frictional, a quiet revolution enabled by experimentation at small scale.

Lessons for the Industry

For insurers, the sandbox has proven to be more than just a compliance tool; it’s a risk-managed innovation engine. Traditional insurers can now test ideas without worrying about the legal complexities of early market deployment. They also benefit from working with startups in a supervised framework, creating real innovation partnerships rather than mere vendor relationships.

For insurtechs, the sandbox has lowered the entry barrier to working with regulated entities. It allows them to prove their product’s viability, establish trust with insurers, and use real-world metrics to attract future investment or scale. For many, it has been the difference between concept and commercialisation.

For regulators, the biggest takeaway is that policy can become iterative. Instead of creating sweeping rules for untested ideas, IRDAI has used the sandbox to collect real-world feedback. That insight has directly shaped regulatory evolution. It also reinforces the idea that modern regulation doesn’t mean deregulation it means flexible, principle-based frameworks that evolve with market needs.

What the 2025 Framework Changes

With growing industry interest and evolving use cases, IRDAI has now introduced a revised Regulatory Sandbox Framework for 2025. The new structure is more scalable and responsive. It removes rigid timelines in favour of project-specific durations (up to 36 months in complex cases), allows cross-sector sandboxes (for products touching finance, health, or payments), and tightens data protection and consent architecture in alignment with India’s data privacy laws.

These changes reflect maturity not only of the regulator, but of the ecosystem that’s now ready to take bigger, more integrated bets. The sandbox is no longer a pilot project it is now part of the regulatory operating model for insurance innovation.

The Road Ahead

Looking forward, IRDAI’s sandbox will be central to how India embraces the next generation of insurance products. Whether it’s parametric insurance for climate risk, real-time claims using AI, or embedded policies linked to digital commerce, the sandbox is now the proving ground.

Its success will depend on continued regulatory clarity, stronger ecosystem collaboration, and deeper integration with India’s digital public infrastructure ABDM, Aadhaar, Account Aggregator, and beyond. But what’s clear is that the sandbox has already redefined how insurers approach innovation.

For a sector often seen as conservative, the sandbox has provided a new permission structure: one where creativity isn’t just allowed it’s expected, encouraged, and made scalable.

Recent Posts

Related Posts

AI Claims Automation in Insurance: Faster Settlements, Higher Trust

Insurance Transparency: Why Trust Is the New Technology in Insurance

Usage-Based Motor Insurance & Telematics in India: The Next Wave

AI-Powered Compliance: How RegTech is Transforming Insurance Governance

DPDPA Meets AI: Regulating the Future of Intelligent Insurance