Data Privacy & Insurance

DPDPA in Indian Insurance: Privacy-Led Innovation Guide

How insurers can turn DPDPA into a competitive advantage by building privacy-first architecture across journeys, data, and partnerships.

India’s insurance landscape is undergoing a massive shift, and multiple transformations can be seen in the insurance segment in terms of products, distribution, business models, and more. Data usage has also continued to increase in this segment due to changing dynamics. If you’ve ever renewed your car insurance or bought a new car, you’ve likely been approached with calls and emails complete with renewal proposals containing all your details from a dozen insurance providers, most of whom you’ve never interacted with. Sometimes, your existing insurer might not even be among them.

This kind of data sharing has become normal, but it’s precisely what the Digital Personal Data Protection Act (DPDPA) aims to address.

As insurers go digital, data has become their greatest asset and their biggest risk. DPDPA sets the foundation to ensure this transformation happens responsibly.

How the Insurance World is Changing

From Policy-Centric to Experience-Centric

Insurance was earlier treated as a standalone product, sold mostly through agents and revisited only during claims or renewal. Now, it’s integrated into everyday digital journeys. When booking flights on MakeMyTrip, for instance, travel insurance is auto-added during checkout via ICICI Lombard or Tata AIG where no extra steps are needed.

From Agent-Driven Sales to Embedded Platforms

Distribution has been transitioning from agents and branches to in-app journeys. Platforms like Flipkart, Paytm, and Ola offer insurance right when customers need it. PhonePe offers health insurance during UPI transactions, while Flipkart and Bajaj Allianz bundle device protection at checkout.

From Static Pricing to Real-Time, Usage-Based Models

Instead of fixed premiums, insurers now use real-time data to personalize pricing. Kotak’s Pay-As-You-Drive plan, for example, calculates motor insurance based on driving behavior tracked via sensors.

From Manual Claims to AI-Led Claims

Claims that once took days and paperwork can now be settled in minutes. Lemonade, in the US, processes some claims via chatbot in under three minutes. In India, Digit uses AI and photo uploads to fast-track approvals.

Catalysts Behind the Digital Transformation

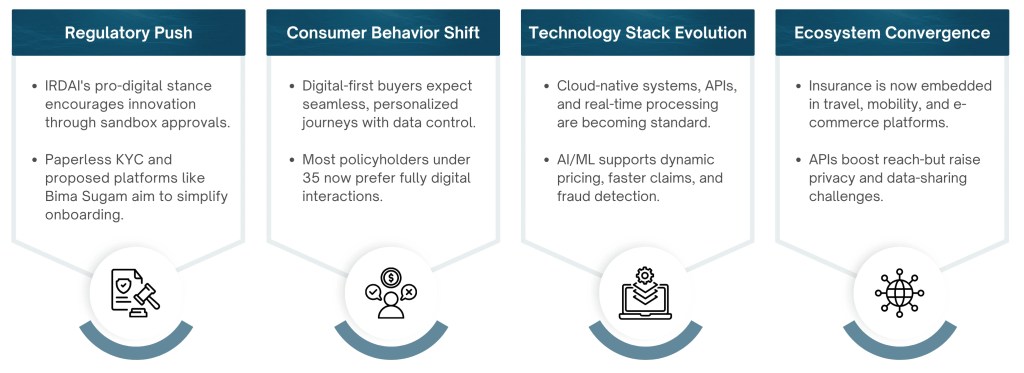

The shift in India’s insurance landscape isn’t just organic, it’s being actively driven by multiple enablers. Regulatory reforms, changing customer expectations, evolving tech stacks, and cross-industry partnerships are pushing insurers to innovate at scale.

- Regulatory Push: IRDAI reforms the sandbox experiments, proposed Bima Sugam, and eKYC to promote digital-first innovation.

- Customer Behavior Shift: Gen Z and millennials expect hyper-personalized, frictionless, and fully digital journeys.

- Technology Stack Evolution: Cloud-native cores, APIs, and real-time processing drive AI-led pricing and claims.

- Ecosystem Convergence: Insurers now operate through retail, mobility, travel, and fintech platforms via APIs.

Operationalizing DPDPA: The Five-Pillar Framework

To turn DPDPA into day-to-day practice, insurers must focus on five core capabilities:

1. Consent Architecture Redesign

Move from static checkboxes to real-time, contextual consent flows to build into apps, agent journeys, and digital portals.

2. Comprehensive Data Mapping

Trace sensitive data across platforms: CRM, underwriting, claims, legacy systems. Understand where it’s stored, how it’s used, and where it flows.

3. Privacy by Design Integration

Run DPIAs before launching AI-based underwriting, wearables-led products, or new partner APIs. Identify risks before they become liabilities.

4. Breach Response Protocols

Set up detection tools, response playbooks, and regulator notification processes to meet DPDPA’s tight timelines.

5. Third-Party Data Governance

Audit brokers, TPAs, aggregators, and SDK vendors. Make sure contracts, logs, and security controls are DPDPA-aligned.

Use Cases: Emerging Insurance Models & DPDPA Risk

1. Usage-Based Insurance & IoT

Insurers now offer real-time pricing based on driver behavior, wearable data, and smart devices. Data like GPS, driving habits, heart rate, and home sensors is captured. Key risks include purpose creep, profiling without user knowledge, and offshore data storage.

2. Pay-as-You-Use Motor Insurance

This model allows users to pay insurance premiums based on their selected usage slab, typically ranging from 2,500 to 7,500 kilometers. Insurers have either launched or are in the process of launching such products, linking premiums directly to vehicle usage. Data collected includes trip logs, GPS information, and phone sensor activity. However, risks emerge around profiling and the fact that consent is captured via the app and is not always revocable.

3. Embedded Insurance in App Journeys

Insurance is bundled with purchases or rides and issued instantly. Data includes flight, ride, device, and invoice metadata. Privacy concerns include lack of opt-out, bundled consent, and unclear fiduciary responsibility.

4. Digital Aggregators

Users can compare and buy policies across insurers. Platforms collect PAN, Aadhaar, call logs, and document scans. Hybrid flows lead to fragmented consent logs, but liability still rests with insurers.

5. API-led POS Distribution

New age Insurance-As-A-Service providers enable insurance sales at retail checkout (e.g., Croma, Ola). Data like IMEI, contact, SKU, and consent toggles are collected. Consent is handled by partners, risking poor audit trails and shared accountability.

6. Hybrid & Digital-Only Models

Insurers use paper, call, app, and API-based journeys. They collect KYC, clickstream, and call data. With no central consent registry, withdrawals are often manual or missing, posing compliance gaps.

DPDPA Obligations in a Changing Insurance Ecosystem

Obligations include:

- Consent traceability across all platforms

- Purpose limitation tags on all data usage

- Clear withdrawal and erasure workflows

- Cross-border restrictions and audit readiness

- Role-based access controls

How Insurance Players Should Get Ready for Compliance

- Insurers should run DPDPA gap assessments across customer journeys, systems, and departments to identify non-compliant areas.

- Build consent infrastructure that ensures traceability, revocability, and works seamlessly across all digital and offline channels.

- Train internal stakeholders beyond legal teams including product, tech, and sales teams to understand and manage privacy risks.

- Update third-party SLAs to include DPDPA clauses, audit rights, and breach notification obligations across partner ecosystems.

Conclusion

Recent Posts

Related Posts

Usage-Based Motor Insurance & Telematics in India: The Next Wave

AI-Powered Compliance: How RegTech is Transforming Insurance Governance

DPDPA Meets AI: Regulating the Future of Intelligent Insurance

DPDPA Insurance India: Data Privacy in Insurance

RegTech & Compliance: The Future of Digital Insurance in India