Insurance

Usage-Based Motor Insurance & Telematics in India: The Next Wave

India’s motor insurance market is shifting gears. Telematics and usage-based models are redefining how premiums are priced making coverage more transparent, personalised, and driven by real-world behaviour.

Rethinking Motor Insurance for the Real World

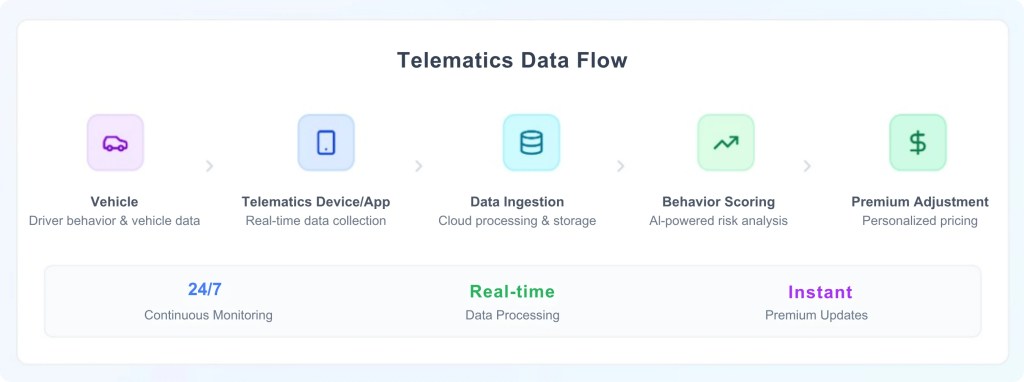

India’s motor insurance industry is undergoing a quiet but radical transformation. Traditional pricing models, based on general assumptions like vehicle type or age, are being challenged by a new approach Usage-Based Insurance (UBI). Powered by telematics, UBI ties premiums to how much and how well people actually drive. In an age where hybrid work, rising fuel costs, and shifting urban mobility trends are changing the way Indians use their vehicles, this model offers not just fairness but flexibility. For both insurers and policyholders, it represents a more accurate and rewarding way to manage risk.

Several factors are driving this shift. The technical infrastructure smartphones, affordable sensors, mobile data has matured enough to support widespread telematics adoption. Consumers are increasingly looking for personalised, tech-forward insurance experiences. Meanwhile, IRDAI has taken visible steps to create space for innovation by approving PAYD and PHYD products and expanding regulatory sandbox participation. In this environment, insurers are no longer wondering whether to test UBI they’re strategizing how to scale it.

From Pilots to Product: The Emergence of UBI Models

Adoption Realities and Strategic Shifts

The Indian consumer is not yet sold on UBI, but the interest is growing. Younger, urban policyholders especially those familiar with shared mobility and digital wallets are more open to behavioural pricing. But concerns about privacy, data misuse, and unclear reward structures persist. This puts the onus on insurers to design experiences that are not only compliant but compelling. Consent needs to be transparent, the value exchange clear, and the onboarding process seamless. If trust is earned at this stage, it can drive long-term retention.

The rise of UBI also brings implications for the broader insurance ecosystem. OEMs are fast becoming distribution allies, embedding insurance products into the vehicle purchase journey. Agents and brokers must evolve from sales-focused intermediaries to advisors who help customers understand driving scores, policy adjustments, and data rights. Underwriting and product development teams are shifting from annual renewal cycles to continuous data-driven calibration. Even claims handling is being reimagined, as real-time vehicle data helps validate accident reports or detect fraud more precisely.

The Road Forward: Data, Infrastructure, and Possibility

For UBI to succeed at scale, insurers must invest in the right digital infrastructure. Telematics data whether captured through apps or devices must flow securely into AI engines capable of translating raw behaviour into underwriting insights. These systems need to be interoperable with policy admin tools, regulatory reporting platforms, and customer engagement dashboards. With the introduction of India’s Digital Personal Data Protection Act (DPDPA), compliance is now a board-level responsibility, and insurers must bake privacy and consent safeguards into every layer of their tech stack.

A Shift in Mindset, Not Just in Models

UBI represents more than a new underwriting tool it marks a cultural shift in how we perceive insurance. When customers understand that their behaviour directly influences their costs and benefits, they begin to see insurers not as passive protectors, but as active partners in their safety. For the industry, this is a rare opportunity to move closer to its customers, improve its risk intelligence, and differentiate on trust and transparency. If embraced thoughtfully, usage-based motor insurance can set the tone for a new era of intelligent, equitable, and responsive coverage.

Recent Posts

Related Posts

Usage-Based Motor Insurance & Telematics in India: The Next Wave

AI-Powered Compliance: How RegTech is Transforming Insurance Governance

DPDPA Meets AI: Regulating the Future of Intelligent Insurance

DPDPA Insurance India: Data Privacy in Insurance

RegTech & Compliance: The Future of Digital Insurance in India