AI Claims Automation in Insurance: Faster Settlements, Higher Trust

AI claims automation is transforming insurance in India. Learn how AI-driven claims processing improves speed, reduces fraud, and enhances customer trust.

Insurance Transparency: Why Trust Is the New Technology in Insurance

Insurance transparency is becoming critical in the age of AI-driven underwriting and claims. Learn why trust is emerging as the defining advantage for insurers in India.

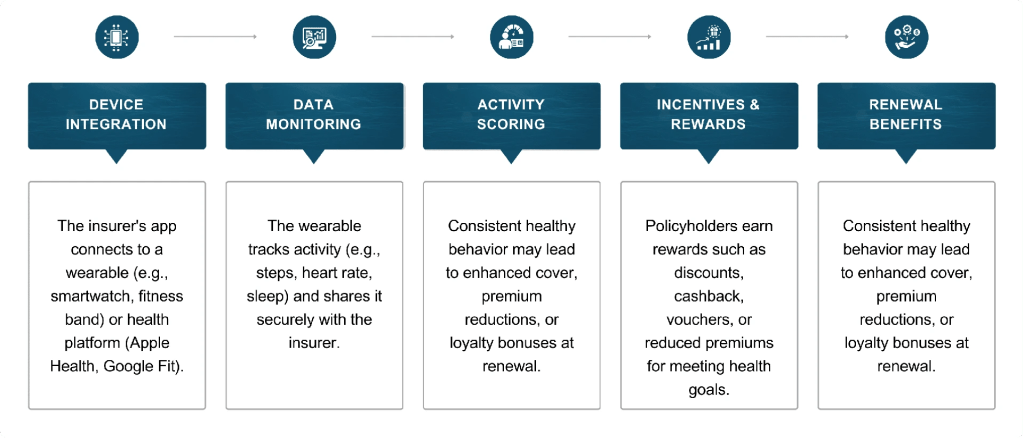

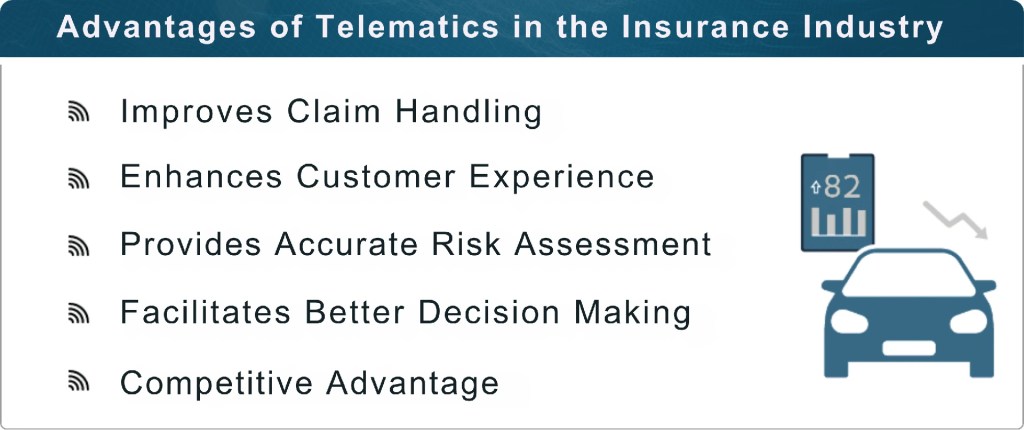

Usage-Based Motor Insurance & Telematics in India: The Next Wave

Telematics and data-driven pricing are transforming India’s motor insurance bringing fairer, personalised, and smarter coverage for modern drivers.